Earned income tax credit

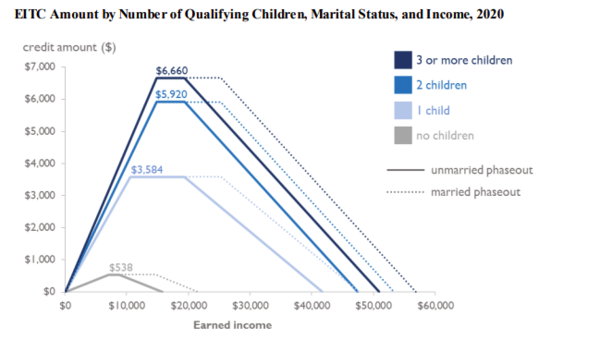

[4] The earned income tax credit has been part of political debates in the United States over whether raising the minimum wage or increasing EITC is a better idea.[11] Upon enactment, the EITC gave a tax credit to individuals who had at least one dependent, maintained a household, and had earned income of less than $8,000 during the year.[13] Today, the EITC is one of the largest anti-poverty tools in the United States,[14] and is mainly used to "promote and support work".And a person classified as "permanently and totally disabled" (one year or more) can be any age and count as one's qualifying "child" provided the other requirements are met.Parents claim their own child(ren) if eligible unless they are waiving this year's credit to an extended family member who has higher adjusted gross income.[16][17] In the 2009 American Recovery and Reinvestment Act, the EITC was temporarily expanded for two specific groups: married couples and families with three or more children; this expansion was extended through December 2012 by H.R.Effective for the 2010, 2011, 2012 and 2013 filing seasons, the EITC supported these taxpayers by: As of 2022, 30 states and DC have enacted state EITCs: California, Colorado, Connecticut, Delaware, District of Columbia, Hawaii, Illinois, Indiana, Iowa, Kansas, Louisiana, Maine, Maryland, Massachusetts, Michigan, Minnesota, Montana, Nebraska, New Jersey, New Mexico, New York, Ohio, Oklahoma, Oregon, Rhode Island, South Carolina, Vermont, Virginia, Washington, and Wisconsin.For example, in an extended family situation, both a parent and an uncle may meet the initial standards of relationship, age, and residency to claim a particular child.[17] A single parent younger than age 19 living in an extended family situation is potentially claimable as the qualifying "child" of an older relative.And a single parent under age 24 who is also a full-time college student (one long semester or equivalent) living in an extended family situation is also potentially claimable.That is, the young adult who is full-time for at least part of five different months can be 23 years and 364 days on December 31 and meet the age requirement to be someone else's qualifying "child."U.S. military personnel stationed outside the United States on extended active duty are considered to live in the U.S. for purposes of the EIC.Temporary absences, for either the claimant or the child, due to school, hospital stays, business trips, vacations, shorter periods of military service, or jail or detention, are ignored and instead count as time lived at home.[16] "Temporary" is perhaps unavoidably vague and generally hinges or whether the claimant and/or the child are expected to return, and the IRS does not provide any substantial guidance past this.[30] As a result of the American Rescue Plan Act of 2021, the investment income limit was increased to $10,000 effective the 2021 tax year and will be adjusted for inflation.[33] In addition, if a person obtains a divorce by December 31, that will carry, since it is marital status on the last day of the year that controls for tax purposes.These EITC dollars had a significant impact on the lives and communities of the nation's lowest-paid working people largely repaying any payroll taxes they may have paid.Haskell (2006) finds that the unique spending patterns of lump-sum tax credit recipients and the increasingly global supply chain for consumer goods is counter-productive to producing high, localized multipliers.However, Haskell points to a silver lining: there are perhaps more important benefits from recipients who use the credit for savings or investment in big-ticket purchases that promote social mobility, such as automobiles, school tuition, or health-care services.Single, Head of Household, and Qualifying Widow(er) are all equally valid and eligible filing statuses for claiming EITC.The EITC may explain why the United States has high levels of maternal employment, despite the absence of childcare subsidies or parental leave.[49] Many nonprofit organizations around the United States, sometimes in partnership with government and with some public financing, have begun programs designed to increase EITC utilization by raising awareness of the credit and assisting with the filing of the relevant tax forms.[50] The state of California requires employers to notify every employee about the EITC every year, in writing, at the same time W-2 forms are distributed.The combination of Earned Income Credit, RALs, and RACs has created a major market for the storefront tax preparation industry.The tax preparation industry responded that at least one-half of RAL customers included in the IRS data actually received RACs instead.Advertisement phrases such as "Rapid Refund" have been deemed deceptive and illegal, since these financial products do not speed remittances beyond the routine automation of tax return processing, and do not make it clear that these are loan applications.Beginning with 2011 tax season, the IRS announced that they would no longer provide preparers and financial institutions with the “debt indicator” that assisted banks in determining whether RAL applications were approved.[60][61] However, a March 2013 article in CNN Money reported that tax prep companies are offering a hodgepodge of financial products similar to RALs.

tax creditmeans-testedMedicaidTemporary Assistance for Needy FamiliesAmerican Economic AssociationRichard NixonFamily Assistance Plannegative income taxGeorge McGoverndemograntRussell LongGerald FordTax Reduction Act of 1975Tax Reform Act of 1986American Recovery and Reinvestment ActTax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010CaliforniaColoradoConnecticutDelawareDistrict of ColumbiaHawaiiIllinoisIndianaKansasLouisianaMarylandMassachusettsMichiganMinnesotaMontanaNebraskaNew JerseyNew MexicoNew YorkOklahomaOregonRhode IslandSouth CarolinaVermontVirginiaWashingtonWisconsinSan FranciscoNew York CityMontgomery County, MarylandInternal Revenue CodesalariesAmerican Rescue Plan Act of 2021minimum wageparental leaveentitlement spendingCapital gains taxChild tax credit (United States)Guaranteed minimum incomeRefund anticipation loanTaxation in the United StatesUnearned incomeSteuerle, C. EugeneNational Tax AssociationSouthern Economic AssociationTax Policy CenterMaking Work Pay CreditThe Washington TimesWayback MachineCiteSeerXHouse Ways and Means CommitteeCongressional Research ServiceBrookings Institution